Introduction

Employee fraud poses a significant threat to businesses, leading to financial losses and reputational damage. To effectively combat this issue, it is crucial to understand the underlying motivations that drive individuals to engage in fraudulent activities. The Fraud Triangle, a concept introduced by criminologist Donald R. Cressey, provides a framework for comprehending the factors that contribute to the occurrence of occupational fraud. By identifying and addressing these factors, businesses can create a culture of integrity and minimize the risk of fraudulent behavior.

What is the Fraud Triangle?

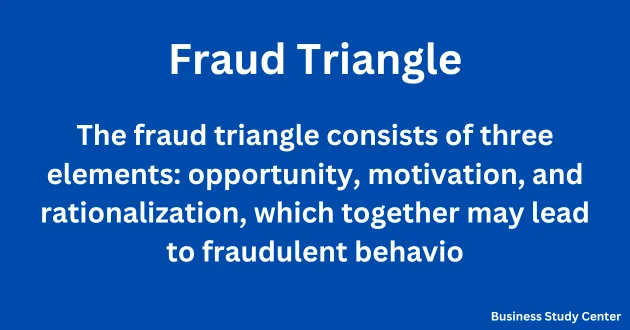

The Fraud Triangle is a model that explains the reasoning behind an individual’s decision to commit fraud. It outlines three key components: opportunity, motivation, and rationalization. According to the Fraud Triangle theory, when these three elements converge, the likelihood of occupational fraud increases significantly. Let’s delve deeper into each component of the Fraud Triangle to gain a comprehensive understanding of its implications.

The Components of the Fraud Triangle

- Opportunity: This component refers to the circumstances that allow fraud to occur within an organization. Businesses have control over the opportunity factor, as they can implement robust internal controls and establish clear policies and procedures to minimize the risk of fraud.

- Motivation: Motivation refers to the driving force behind fraudulent behavior. It encompasses various factors, such as financial pressure, personal grievances, or a desire for personal gain. Understanding the different motivations for fraud is crucial in developing effective prevention strategies.

- Rationalization: Rationalization involves justifying fraudulent actions to oneself. Fraudsters often convince themselves that their behavior is acceptable or justified under certain circumstances. By addressing rationalization and promoting a culture of ethical decision-making, businesses can discourage fraudulent behavior.

Understanding Fraud

Before we delve further into the components of the Fraud Triangle, let’s clarify the concept of fraud itself. Fraud refers to intentional deception carried out by individuals or organizations for personal gain. It involves the manipulation of financial information or the misappropriation of assets, resulting in harm to the organization and benefiting the perpetrator. By comprehending the nature of fraud, businesses can better grasp the importance of the Fraud Triangle in preventing and mitigating fraudulent activities.

Motivation: The Driving Force Behind Fraud

Motivation plays a pivotal role in the occurrence of employee fraud. While not all employees may be predisposed to commit fraud, certain circumstances and pressures can push individuals towards fraudulent behavior. Understanding the various motivations behind fraud is essential in identifying potential risks and implementing appropriate preventive measures.

Types of Motivation

Fraudulent behavior can stem from different types of motivation. Some common motivations for employee fraud include:

- Financial Pressure: Financial difficulties, such as mounting debts, unexpected expenses, or a desire for a higher standard of living, can drive individuals to commit fraud. Employees facing significant financial burdens may view fraud as a means to alleviate their financial stress.

- Personal Grievances: Feelings of being wronged, such as being passed over for promotions or experiencing unfair treatment, can lead employees to rationalize fraud as a form of retribution. These personal grievances can create a sense of entitlement and justification for fraudulent actions.

- Survival: Extreme circumstances, such as a medical crisis or the need to provide for one’s family, can push otherwise honest individuals towards fraudulent behavior. The perceived necessity to secure resources or meet urgent needs can override ethical considerations.

- Status Pressure: The desire to maintain a certain lifestyle or keep up with peers’ financial achievements can contribute to the motivation for fraud. The pressure to appear successful and affluent may lead individuals to engage in fraudulent activities to sustain their desired standard of living.

By understanding the motivations behind employee fraud, businesses can tailor their prevention strategies to address these underlying factors. Creating a supportive and empathetic work environment, providing financial assistance programs, and promoting work-life balance can help alleviate financial pressures and reduce the likelihood of fraudulent behavior.

Opportunity: Creating Conditions for Fraud

Opportunity is a critical component of the Fraud Triangle, as it refers to the circumstances that allow fraud to occur within an organization. While businesses cannot control an individual’s motivations, they have the ability to minimize the opportunity for fraud through the implementation of robust internal controls and risk management practices.

The Importance of Strong Internal Controls

Strong internal controls serve as a fundamental deterrent against employee fraud. They provide a system of checks and balances that mitigate the risk of fraud by imposing strict protocols and ensuring accountability. Key measures to enhance internal controls include:

- Separation of Duties: Implementing a system where multiple employees are involved in critical processes helps prevent any single individual from having too much control or authority over financial transactions. By dividing responsibilities, businesses reduce the risk of fraudulent activities going undetected.

- Regular Audits and Reviews: Conducting periodic audits and reviews enables businesses to identify any irregularities or discrepancies in financial records. These assessments should be performed by independent parties or internal audit teams to ensure objectivity and thoroughness.

- Monitoring and Reporting Systems: Establishing robust monitoring and reporting systems allows businesses to detect fraudulent activities promptly. This includes implementing advanced fraud detection software, setting up anonymous reporting channels, and encouraging employees to report any suspicious behavior.

By proactively addressing the opportunity component of the Fraud Triangle, businesses can significantly reduce the likelihood of fraudulent activities. Regular assessments of internal controls, continuous monitoring, and prompt action in response to identified weaknesses are crucial in maintaining a strong defense against employee fraud.

Rationalization: Justifying Fraudulent Behavior

The final component of the Fraud Triangle is rationalization. Fraudsters often find ways to justify their fraudulent actions, convincing themselves that their behavior is acceptable under certain circumstances. Addressing rationalization is crucial in preventing fraudulent behavior within an organization.

Promoting a culture of ethics and integrity is key to countering rationalization. By fostering an environment where open communication and ethical decision-making are valued, businesses can discourage employees from rationalizing fraudulent actions. Key strategies to address rationalization include:

- Ethical Training Programs: Providing comprehensive ethics training programs equips employees with the necessary knowledge and skills to make ethical decisions. These programs should emphasize the importance of integrity, the consequences of fraudulent behavior, and the benefits of ethical conduct.

- Enhancing Transparency and Communication: Promoting transparency in financial matters and openly communicating the organization’s values and ethical standards helps create a culture of integrity. When employees understand the ethical implications of their actions and witness the organization’s commitment to ethical behavior, they are less likely to rationalize fraudulent actions.

- Implementing Robust Internal Controls: As discussed earlier, strong internal controls play a crucial role in preventing fraud. By implementing and consistently enforcing rigorous control measures, businesses send a clear message that fraudulent behavior will not be tolerated.

By proactively addressing the rationalization component of the Fraud Triangle, businesses can create a work environment that values ethics and integrity, reducing the likelihood of employees engaging in fraudulent activities.

Preventing Employee Fraud

Preventing employee fraud requires a comprehensive approach that encompasses various strategies and measures. By combining the insights gained from understanding the Fraud Triangle with best practices in fraud prevention, businesses can effectively mitigate the risk of fraudulent behavior within their organizations. Let’s explore some key strategies for preventing employee fraud.

Developing Ethical Training Programs

Ethical training programs are instrumental in shaping employees’ understanding of ethical behavior and the consequences of fraud. These programs should emphasize the importance of integrity, the company’s zero-tolerance policy towards fraudulent activities, and the potential legal and reputational consequences of engaging in fraudulent behavior. Regular ethical training sessions, workshops, and ongoing communication reinforce the organization’s commitment to ethical conduct.

Enhancing Transparency and Communication

Promoting transparency and open communication within the organization serves as a powerful deterrent against employee fraud. When employees feel comfortable reporting suspicious behavior, and when there is a clear reporting mechanism in place, potential fraudulent activities can be detected and addressed promptly. Establishing whistleblower hotlines, anonymous reporting channels, and fostering a culture of trust and accountability are essential in maintaining transparency and preventing fraud.

Implementing Robust Internal Controls

As discussed earlier, strong internal controls are critical in preventing employee fraud. These controls should include segregation of duties, regular audits, monitoring systems, and clearly defined policies and procedures. By implementing and consistently enforcing these controls, businesses create an environment that minimizes the opportunity for fraudulent activities and ensures accountability.

Identifying Fraudulent Behavior

Despite preventive measures, it is essential for businesses to remain vigilant and proactive in identifying potential fraudulent behavior. By recognizing warning signs and conducting regular audits and reviews, businesses can detect fraudulent activities at an early stage and take appropriate action. Let’s explore some key strategies for identifying fraudulent behavior.

Recognizing Warning Signs

Certain behavioral and financial indicators may suggest the presence of fraudulent activities. These warning signs include:

- Unexplained financial discrepancies or irregularities in financial records

- Frequent and unexplained changes in an employee’s lifestyle or financial status

- Excessive control or secrecy over financial matters by a single individual

- Unusual or unexplained transactions or expenses

- Complaints from customers or suppliers regarding financial discrepancies or unethical behavior

Business owners and managers should remain vigilant and promptly investigate any red flags or suspicious activities. Timely action can help mitigate the potential damage caused by fraudulent behavior.

Conducting Regular Audits and Reviews

Regular audits and reviews are essential in detecting and preventing employee fraud. These assessments should be conducted by internal or external auditors and should cover financial statements, internal controls, and adherence to established policies and procedures. By conducting frequent audits, businesses can identify any loopholes or weaknesses in their systems and take corrective measures.

The Role of Insurance in Fraud Prevention

While preventive measures are crucial in mitigating the risk of employee fraud, it is also essential to have appropriate insurance coverage to safeguard against potential losses. Crime insurance, specifically designed to address fraud-related risks, can provide financial protection in the event of employee fraud. By obtaining comprehensive crime insurance coverage, businesses can minimize the financial impact of fraudulent activities and ensure business continuity.

Case Studies: Real-Life Examples of the Fraud Triangle

To illustrate the practical implications of the Fraud Triangle, let’s explore a few real-life examples of employee fraud and how the components of the Fraud Triangle contributed to these incidents. These case studies shed light on the importance of understanding the motivation, opportunity, and rationalization behind fraudulent behavior.

- Case Study 1: The Pressure of Financial Difficulties

In this case, an employee facing significant financial pressure due to mounting debts and family obligations succumbed to the temptation of committing fraud. The opportunity arose when the employee was entrusted with handling financial transactions and had access to sensitive financial information. The employee rationalized their actions by convincing themselves that their fraudulent activities were necessary to alleviate their financial stress.

- Case Study 2: Rationalization through a Sense of Entitlement

In this scenario, an employee who felt overlooked for promotions and raises developed a sense of entitlement and resentment towards the organization. The opportunity for fraud presented itself when the employee was granted access to financial resources without adequate oversight. The employee rationalized their fraudulent behavior by justifying it as retribution for perceived mistreatment.

By analyzing these case studies, business owners can gain valuable insights into the factors that contribute to employee fraud and develop targeted strategies to prevent similar incidents within their organizations.

Conclusion

Employee fraud is a persistent and costly issue that can significantly impact businesses. The Fraud Triangle provides a valuable framework for understanding the motivations, opportunities, and rationalizations that drive individuals to engage in fraudulent activities. By addressing each component of the Fraud Triangle, businesses can implement effective preventive measures, create a culture of integrity, and reduce the risk of employee fraud. Through a combination of ethical training programs, strong internal controls, open communication, and proactive detection measures, businesses can safeguard their financial well-being and protect their reputation from the damaging effects of employee fraud.