Accounting, often called the “language of business,” plays a critical role in the financial world. But what exactly is accounting? Put simply, it’s a systematic and comprehensive process of recording financial transactions pertaining to a business. In this blog post, we’ll delve deeper into the definition of accounting, exploring its varied types, key principles, and the essential financial statements generated through this process. Whether you’re a fledgling entrepreneur, an established business owner, or a budding accountant, gaining insight into these fundamental topics will empower you to make informed financial decisions. Join us as we unravel the intricacies of accounting.

What is Accounting?

Accounting is a fundamental aspect of any business or organization. It involves the process of recording, classifying, summarizing, and interpreting financial transactions to provide useful information for decision-making. In simple terms, accounting can be described as the language of business.

There are various definitions of accounting from different perspectives. From a legal viewpoint, it refers to the preparation and presentation of financial statements in accordance with laws and regulations. From an economic perspective, it is the analysis and communication of financial information to various stakeholders.

Accounting has been around for centuries, evolving from simple record-keeping methods to more sophisticated systems with the advancement of technology. It is an essential tool for businesses to measure their performance, plan for the future, and comply with tax laws.

How Accounting Works

The primary purpose of accounting is to provide accurate and reliable financial information about a business or organization. This is achieved by following certain principles, standards, and procedures set by governing bodies such as the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB).

Accounting works through a series of steps known as the accounting cycle. It starts with identifying and recording financial transactions in a general ledger. The transactions are then classified into different accounts, such as assets, liabilities, equity, revenues, and expenses. This process is known as double-entry bookkeeping.

After the transactions have been recorded and classified, they are summarized in financial statements. These statements include the balance sheet, income statement, and cash flow statement. These reports provide an overview of the financial position, performance, and cash flow of a business.

Why Accounting is Important

Accounting is essential for businesses because it helps in decision-making, financial planning, and monitoring performance. It also provides information to external stakeholders such as investors, lenders, and government agencies.

By keeping track of financial transactions and preparing accurate reports, accounting allows businesses to analyze their profitability, identify areas for improvement, and make informed decisions. It also helps in setting financial goals, creating budgets, and managing cash flow effectively.

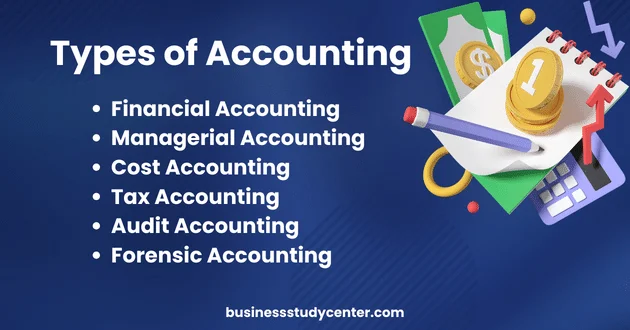

Types of Accounting

There are many types of accounting, each with its unique focus and purpose. Let’s explore a few of the most common ones.

Financial Accounting

Financial accounting involves recording, summarizing, and reporting financial transactions and information to external stakeholders such as investors, creditors, and government agencies. These stakeholders use this information to make decisions regarding their involvement with the company.

Financial statements, including the balance sheet, income statement, and cash flow statement, are the primary outputs of financial accounting. These statements provide a snapshot of the company’s financial performance, position, and cash flow at a specific point in time.

Managerial Accounting

Managerial accounting is used to provide information and analysis to internal stakeholders within a company, such as management and decision-makers. This type of accounting focuses on providing timely and relevant data for planning, controlling, and evaluating business operations.

Managerial accounting reports may include budgeting, cost analysis, and performance evaluation information that can help managers make informed decisions to improve the company’s financial performance.

Cost Accounting

Cost accounting focuses on determining and analyzing the costs associated with producing goods or services. This information is essential for companies to make pricing decisions, manage expenses, and evaluate profitability.

This type of accounting may involve calculating direct costs (such as materials and labor) and indirect costs (such as overhead) to determine the total cost of production per unit. Cost accountants also analyze variances between actual costs and budgeted costs to identify areas for improvement.

Tax Accounting

Tax accounting specializes in preparing and filing tax returns for individuals and businesses. This type of accounting requires a thorough understanding of tax laws, regulations, and deadlines to ensure compliance with the relevant authorities.

In addition to tax preparation services, tax accountants may also provide advice on strategies to minimize taxes and maximize tax benefits for their clients.

Audit Accounting

Audit accounting involves reviewing and verifying financial statements to ensure their accuracy and compliance with relevant laws, regulations, and accounting standards. This type of accounting is usually performed by external auditors who provide an independent opinion on the company’s financial statements.

Audits can help improve the reliability and credibility of a company’s financial reporting, which can increase stakeholders’ trust and confidence in the company. They also provide valuable insights and recommendations for improving internal controls, risk management, and overall financial health.

Forensic Accounting

Forensic accounting involves using financial information and data analysis techniques to investigate potential fraud or illegal activities within a company. This type of accounting requires specialized skills in accounting, auditing, and investigative procedures to uncover any suspicious activity.

Forensic accountants may be called upon to assist with litigation cases, insurance claims, or internal investigations. They play a crucial role in identifying and preventing fraudulent activities that can have severe consequences for a company’s reputation and financial stability.

Principles of Accounting

Before delving into the intricacies of accounting, it’s crucial to understand the foundational principles that guide all accounting activities. These principles create a standardized framework ensuring consistency, reliability, and comparability across all financial statements and reports. Let’s explore these principles and their importance in detail.

Generally Accepted Accounting Principles (GAAP)

Generally Accepted Accounting Principles (GAAP) are a collection of commonly followed accounting rules and standards for financial reporting. These principles guide accountants and auditors on how to record and report business transactions, ensuring the consistency and comparability of financial information across industries and sectors. GAAP regulations encompass a broad range of accounting practices, from the recognition of revenue and expenses to the treatment of intangible assets.

The Financial Accounting Standards Board (FASB) is the primary body responsible for developing and endorsing GAAP in the United States. Furthermore, the U.S. Securities and Exchange Commission (SEC), which oversees the protection of investors and maintains the integrity of the securities markets, recognizes these principles as authoritative for companies in the U.S.

International Financial Reporting Standards (IFRS)

International Financial Reporting Standards (IFRS) are a set of accounting standards developed by the International Accounting Standards Board (IASB) for the preparation of financial statements. These standards are used in over 120 countries and are becoming the global standard for the preparation of public company financial reports. The primary aim of IFRS is to establish a common language for business affairs so that company accounts are comprehensible and comparable across international boundaries.

One significant difference between IFRS and GAAP is that while GAAP is rule-based, IFRS is principle-based. This means that under IFRS, the focus is on meeting the broader principles of accurate reporting, which can provide more flexibility to companies but may also lead to more subjective interpretations. Under GAAP, by contrast, companies must follow specific, detailed rules when compiling their financial reports.

Another key difference is their geographical usage. While GAAP is primarily used within the United States, IFRS is used in many countries globally. This can impact how companies report their finances, particularly multinational corporations with operations in various countries.

Accrual Basis Accounting

Accrual basis accounting is a method of financial accounting where revenues and expenses are recognized and recorded when they are earned or incurred, regardless of when cash is exchanged. This system is based on the matching principle, which aims to match revenues with the expenses incurred in generating them.

In accrual basis accounting, revenue recognition happens when a sale is made, or a service is provided, not necessarily when payment is received. Similarly, expense recognition takes place when a cost is incurred, not necessarily when it is paid. This system allows for a more accurate portrayal of a company’s financial health by reflecting financial commitments that cash-based accounting might overlook.

Cash Basis Accounting

Cash-based accounting is a financial accounting method that recognizes revenue when cash is received and expenses when they are paid. This method differs dramatically from accrual-based accounting, where revenues and expenses are recognized when they are earned or incurred, regardless of when cash changes hands. This method is more suitable for self-employed individuals or small businesses with simple transactions and can provide a straightforward view of cash flow.

Matching Principle

The matching principle is a fundamental financial accounting concept that states that expenses should be recognized in the same period as the revenues they help generate. This principle ensures that financial statements accurately reflect the financial performance of a company during a specific period.

For example, if a company sells goods and services on credit in one month but receives payment in the following month, both the sale and related expenses should be recorded in the same month to accurately reflect the financial activity during that period.

Financial Statements and Reports

As mentioned earlier, financial statements are the primary outputs of financial accounting. These statements provide valuable information about a company’s financial performance, position, and cash flow to help stakeholders make informed decisions.

Balance Sheet

The balance sheet is a snapshot of a company’s assets, liabilities, and equity at a specific point in time. It follows the basic accounting equation: Assets = Liabilities + Equity. The balance sheet shows what a company owns (assets), what it owes (liabilities), and the owner’s or shareholders’ stake in the company (equity). This statement helps stakeholders understand the company’s financial position and its ability to meet short-term and long-term obligations.

Income Statement

The income statement, also known as the profit and loss statement, shows a company’s revenues and expenses over a specific period. It helps stakeholders understand how much money the company earned (revenue) and how much it spent (expenses) to generate those revenues. The bottom line of the income statement shows the company’s net income or loss for the period. This statement is crucial for assessing a company’s profitability and financial performance.

Statement of Retained Earnings

The statement of retained earnings shows the changes in a company’s retained earnings account over a specific period. Retained earnings represent the accumulated profits or losses that have not been distributed to shareholders as dividends. This statement reconciles the beginning and ending balance of the retained earnings account, including any adjustments such as net income or dividend payments. It helps stakeholders understand how the company’s profits are being used to fund future growth or return value to shareholders.

Cash Flow Statement

The cash flow statement reports the sources and uses of cash during a specific period, providing insights into a company’s liquidity and ability to generate cash. It categorizes cash flows into operating, investing, and financing activities to help stakeholders understand how the company manages its cash. A positive cash flow is essential for a company’s financial health, as it ensures the company can meet its short-term obligations and continue to invest in its operations.

Conclusion

Accounting plays a crucial role in business operations by providing accurate and timely financial information for decision-making. With various types of accounting and financial statements, companies can effectively manage their resources, track performance, and comply with relevant laws and regulations. Whether you’re a business owner, investor, or financial professional, understanding the basics of accounting can help you make informed decisions and contribute to a company’s success.