The accounting equation is the fundamental concept underlying the field of accounting. It serves as the foundation for recording, analyzing, and reporting financial transactions and is essential for understanding the financial health of a business. In this blog post, we will explore what the accounting equation is, how it works, and its significance in financial analysis.

What is the Accounting Equation?

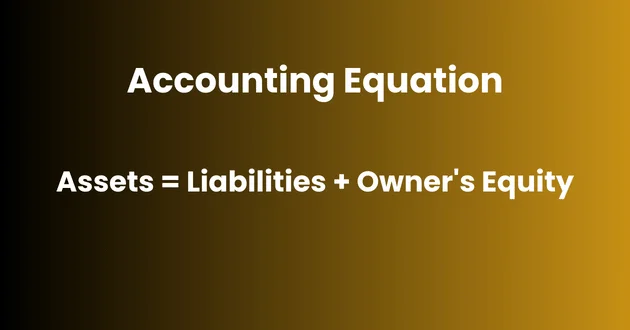

The accounting equation, also known as the balance sheet equation, is a simple mathematical formula that represents the relationship between a company’s assets, liabilities, and owner’s equity. It can be expressed as follows:

Assets = Liabilities + Owner’s Equity

This equation states that a company’s total assets must equal the sum of its liabilities and owner’s equity. In other words, it asserts that everything a company owns (assets) is either funded by external sources (liabilities) or by the owner’s investment (owner’s equity).

The accounting equation is the cornerstone of double-entry bookkeeping, which is the system used to record financial transactions. It ensures that every transaction is properly recorded and balanced. By following this equation, businesses can maintain accurate and reliable financial records.

Understanding the Components of the Accounting Equation

1. Assets:

Assets are economic resources owned or controlled by a company that have measurable value. They can be tangible, such as cash, inventory, or property, or intangible, such as patents or trademarks. Assets represent what a company owns and can use to generate future economic benefits.

For example, cash is an asset because it provides immediate purchasing power and can be used to pay off liabilities or invest in business operations. Inventory is also an asset because it represents goods held for sale and can be converted into cash.

2. Liabilities:

Liabilities are the obligations or debts owed by a company to external parties. These can include loans, accounts payable, or accrued expenses. Liabilities represent the company’s financial obligations that need to be settled in the future.

For instance, if a company takes out a loan to finance its operations, the amount of the loan becomes a liability on its balance sheet. Accounts payable, such as outstanding invoices from suppliers or unpaid bills, are also considered liabilities as they represent amounts owed to external parties.

3. Owner’s Equity:

Owner’s equity, also known as shareholders’ equity or net worth, represents the residual interest in the assets of a company after deducting liabilities. It is the ownership claim on the company’s assets by its owners or shareholders. Owner’s equity increases when owners invest additional capital or when the company generates profits.

When a company earns profits, it can choose to distribute a portion of those profits to its owners as dividends or retain them within the business. Retained earnings increase owner’s equity, reflecting accumulated profits that have not been distributed.

How the Accounting Equation Works

The accounting equation follows the principle of double-entry bookkeeping, which means that every transaction has equal debits and credits. Let’s explore how different transactions impact the accounting equation:

Transaction 1: Purchase of Equipment with Cash

When a company purchases equipment using cash, two accounts are affected:

- Debit: The equipment account increases, representing an increase in assets.

- Credit: The cash account decreases, representing a decrease in assets.

The accounting equation remains balanced because there is an increase in one asset account (equipment) and a corresponding decrease in another asset account (cash).

For example, if a company buys a new computer for $1,000 using cash from its bank account, it would record a debit of $1,000 in the equipment account (increasing its asset value) and a credit of $1,000 in the cash account (decreasing its asset value).

Transaction 2: Obtaining a Bank Loan

When a company obtains a bank loan, there are two accounts involved:

- Debit: The cash account increases, representing an increase in assets.

- Credit: The loan liability account increases, representing an increase in liabilities.

Again, the accounting equation remains balanced as there is an increase in one asset account (cash) and an increase in one liability account (loan).

For instance, if a company secures a bank loan of $10,000, it would record a debit of $10,000 in the cash account (increasing its asset value) and a credit of $10,000 in the loan liability account (increasing its liability value).

Transaction 3: Owner’s Capital Investment

When an owner invests additional capital into their business, two accounts are impacted:

- Debit: The cash account increases, representing an increase in assets.

- Credit: The owner’s equity account increases, representing an increase in owner’s equity.

The accounting equation stays balanced with an increase in both asset (cash) and owner’s equity accounts.

For example, if an owner invests $5,000 of personal funds into their business bank account, it would record a debit of $5,000 in the cash account (increasing its asset value) and a credit of $5,000 in the owner’s equity account (increasing its value).

Transaction 4: Sale of Goods on Credit

When a company sells goods on credit, two accounts are affected:

- Debit: The accounts receivable account increases, representing an increase in assets.

- Credit: The sales revenue account increases, representing an increase in revenue.

The accounting equation remains balanced as there is an increase in one asset account (accounts receivable) and an increase in the revenue account.

For example, if a company sells goods worth $1,000 to a customer on credit, it would record a debit of $1,000 in the accounts receivable account (increasing its asset value) and a credit of $1,000 in the sales revenue account (increasing its revenue).

Transaction 5: Payment of Salaries

When a company pays salaries to its employees, two accounts are impacted:

- Debit: The salary expense account increases, representing an increase in expenses.

- Credit: The cash account decreases, representing a decrease in assets.

The accounting equation remains balanced as there is an increase in one expense account (salary expense) and a corresponding decrease in the cash account.

For instance, if a company pays $5,000 in salaries to its employees, it would record a debit of $5,000 in the salary expense account (increasing its expense) and a credit of $5,000 in the cash account (decreasing its asset value).

Significance of the Accounting Equation

The accounting equation is crucial for several reasons:

1. Ensures Accuracy of Financial Records

By following the accounting equation, businesses can maintain accurate and reliable financial records. If the equation is not balanced, it indicates an error in recording transactions. This balance provides assurance that all financial transactions have been accurately recorded and allows for easy identification and correction of errors.

2. Facilitates Financial Analysis

The accounting equation provides a framework for financial analysis. It allows businesses to assess their financial position by comparing the value of their assets to their liabilities and owner’s equity. By examining these components, analysts can evaluate liquidity (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and overall financial health.

For example, comparing total assets to total liabilities provides insights into how well a business can cover its debts. If liabilities outweigh assets significantly, it may indicate financial distress or insolvency.

3. Supports Decision-Making

Understanding the accounting equation helps business owners make informed decisions about financing options, investments, and growth strategies. It provides insights into how different decisions impact a company’s financial position.

For instance, if a business needs additional funding for expansion plans, analyzing the impact on both liabilities and owner’s equity can help determine whether to seek external financing or consider internal sources such as retained earnings.

Limitations of the Accounting Equation

While the accounting equation is a valuable tool, it has some limitations:

1. Does Not Reflect Market Value

The accounting equation is based on historical cost rather than current market value. Therefore, it may not accurately reflect the true value of assets or liabilities.

For instance, if land was purchased decades ago at a low price but has significantly appreciated in value over time due to market forces, its carrying value on the balance sheet will likely be much lower than its current market value.

2. Excludes Non-Financial Information

The accounting equation focuses solely on monetary transactions and does not consider non-financial factors like reputation, customer loyalty, or intellectual property.

While these non-financial factors play a crucial role in assessing a company’s overall value and prospects for success, they are not captured within the accounting equation framework.

Conclusion

The accounting equation is a fundamental concept in accounting that provides a structured framework for recording and analyzing financial transactions. By understanding how assets, liabilities, and owner’s equity interact, businesses can gain insights into their financial health and make informed decisions. While it has its limitations, the accounting equation remains a critical tool for financial analysis and reporting.